Weekly Rolling 8-Week Cash Forecast (Simple, Non-Model)

A simple weekly 8-week cash forecast that prevents surprises and helps you make decisions before you run into trouble. Includes an Excel template.

📌 Summary

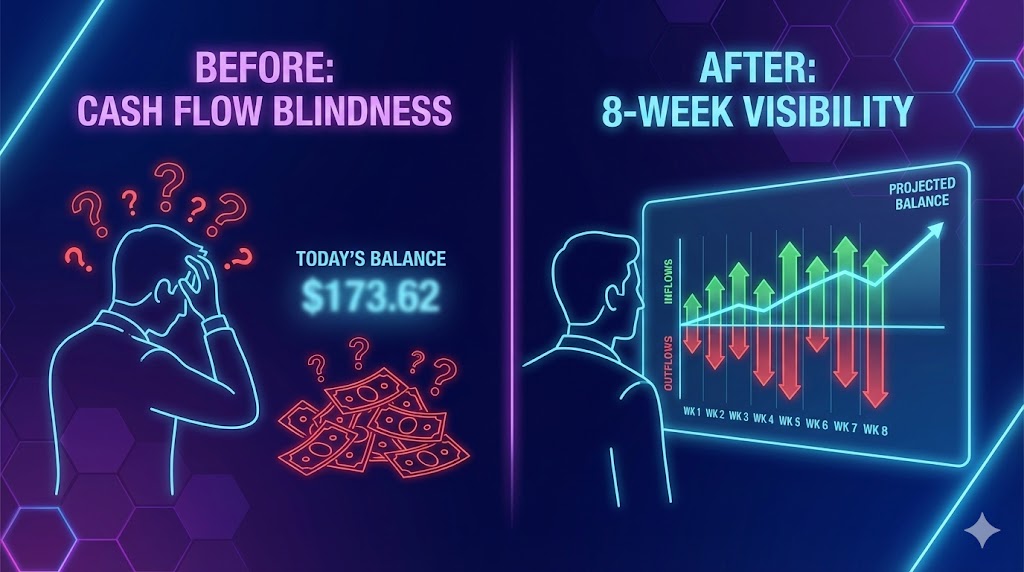

Outcome: You stop being surprised by cash.

Time: 60–90 minutes setup, then 20 minutes/week.

Owner: Finance/Admin owner (or Founder).

Steps: Define buckets → build 8-week view → update weekly → review and act.

Metrics: Weeks of runway, lowest-cash week, forecast vs actual accuracy.

🎯 What you’ll achieve (in 2 weeks)

You’ll know when you’re likely to be tight on cash (before it happens).

You’ll see the real impact of collections, payroll, and big vendor payments.

You’ll have a weekly “money meeting” that produces decisions, not anxiety.

⏱️ Time & effort

Setup: 60–90 minutes

Ongoing: 20 minutes/week

Owner: Finance/Admin owner (or Founder)

Dependencies: Access to bank balance + invoices + upcoming bills/commitments

🚦 When to use this (signals)

Use this quick win if:

Cash surprises happen even when revenue looks fine.

You don’t have a clear view of what’s coming due in the next 30–60 days.

Payroll, taxes, or vendor payments create recurring “panic weeks.”

Spending decisions happen without a forward look.

💰 What this is (and what it isn’t)

This is a cash forecast, not a P&L (Profit and Loss statement), and not a full financial model.

It’s meant to be fast, updated weekly, and good enough to drive decisions.

Precision isn’t the goal. Visibility is.

🧩 Step-by-step (follow in order)

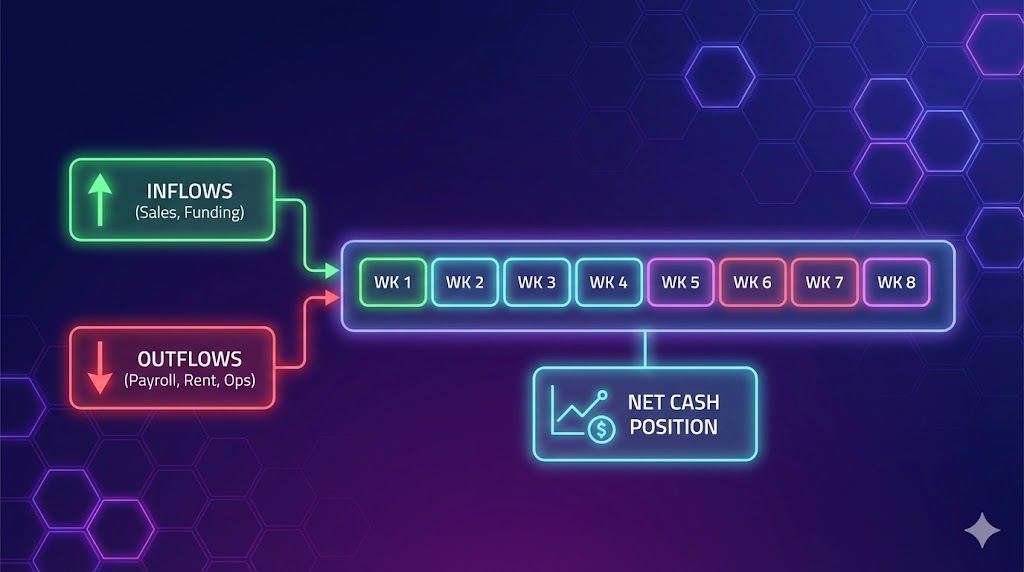

Step 1) Define your “cash in” and “cash out” buckets (keep it short)

Start with 5–8 buckets total.

Cash in (examples)

Collections from customers (invoices due)

New sales expected to close (only if highly likely)

Other income (grants, refunds)

Cash out (examples)

Payroll (including taxes)

Rent / office / fixed ops

Software subscriptions

Vendors / contractors

Taxes

One-off expenses (travel, legal, equipment)

Rule: if you have +15 buckets, you won’t maintain it.

Step 2) List your commitments (the “known future”)

Before forecasting, capture what is already committed:

Payroll dates and amounts

Rent and recurring bills

Vendor invoices due

Tax dates (VAT, payroll taxes, etc.)

Any planned one-offs you already agreed to

This is where most forecasts fail: people forget commitments.

Step 3) Create your 8-week view (one line per week)

For each of the next 8 weeks, estimate:

Starting cash (bank balance)

Cash in (by bucket)

Cash out (by bucket)

Ending cash (starting + in − out)

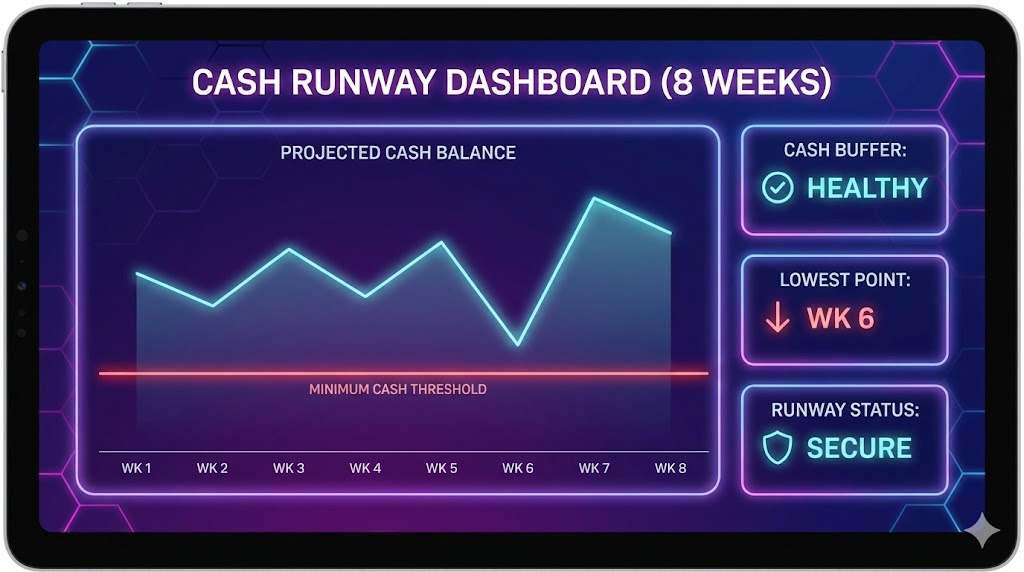

Add one simple rule: Ending cash must never go negative without an action plan.

Step 4) Be conservative about “expected sales”

Only include new sales in cash-in if:

there is a committed deal and a known invoice date and realistic payment terms.

If you’re unsure, put it in a separate “upside” line so it doesn’t hide risk.

Step 5) Update weekly (same day, same time)

Every week (20 minutes):

Replace forecasts with actuals for last week

Update invoice payment dates based on reality

Add any new commitments

Recalculate runway / low-cash weeks

Consistency matters more than detail.

Step 6) Hold a 10-minute “cash review” right after updating

Answer these questions:

What week is the lowest cash point?

What 1–3 actions will prevent a dip? (collect faster, delay spend, renegotiate terms)

What decisions do we need this week?

This turns a spreadsheet into control.

📥 Templates

Use this Excel file to implement the quick win in minutes.

What you’ll get

An 8-week cash view with automatic week dates

Separate lines for Committed cash-in vs Upside (so you don’t hide risk)

Automatic totals + Ending Cash calculations

Alerts when Ending Cash drops below 0 or below your buffer

How to use

Open the file and set Start Date, Starting Cash, and Buffer in Inputs & Lists (blue cells).

Fill weekly Cash In and Cash Out amounts in 8-Week Forecast (blue cells).

Update it weekly: replace last week’s estimates with actuals, then roll forward.

Download:

✅ Done Definition (DoD)

You’re “done” when:

An 8-week forecast exists with simple buckets

All known commitments are listed (payroll, taxes, major bills)

The forecast is updated weekly on a calendar

The team reviews low-cash weeks and takes actions

“Upside” cash-in is separated from committed cash-in

⚠️ Common mistakes (avoid these)

Mistake: Mixing profit with cash → Do this instead: only track cash timing (when money actually moves).

Mistake: Too many categories → Do this instead: 5–8 buckets.

Mistake: Counting “maybe deals” as cash → Do this instead: separate upside.

Mistake: Updating once and forgetting → Do this instead: weekly rhythm, same day.

📈 How to know it’s working (in 2 weeks)

Clarity metric: you can name your lowest-cash week and why

Control metric: fewer last-minute “emergency” decisions

Accuracy proxy: forecast vs actual improves over time (even if imperfect at first)

❓ FAQ

Should I forecast daily instead of weekly?

Weekly is enough for most small businesses. Go daily only if you’re extremely tight on cash.

What if we don’t invoice (we charge cards / ecommerce)?

Use the same structure: forecast cash in based on expected receipts, and include processor payout timing.

What about credit cards and loans?

Include them as cash-in (draws) or cash-out (payments), and list payment dates under commitments.

What if my forecast is always wrong?

That’s normal early on. The goal is to spot risk weeks early, not to predict perfectly. Accuracy improves with repetition.

🔗 Related quick wins

Want this to run automatically?

You can implement this with any tools. If you’re using Super, you can unify invoices, bills, and commitments, and generate an always-updated 8-week cash view in one place.